Is EA Really For Sale and What Does the Metaverse Have to Do With It?

Need for Intellectual Property is Real But Merger Talks May Just Be Virtual Reality

With rumors swirling of Electronic Arts being the latest subject of acquisition and merger speculation, let’s dive into just how real this feels, what permutations exist for combinations and just what the heck the development of the metaverse has to do with it.

Before we dive in, let’s just reset where we are coming from in terms of capital markets activity in the interactive entertainment space to lay the background for why a company like Electronic Arts is now among the rumored merger targets. Despite the covid-19 pandemic and its acute impact on financial markets, 2020 and 2021 were record years for capital markets activity in the entertainment software industry across M&A, IPOs and VC funding. Leading acquirers continued to be aggregators like Embracer, Stillfront and Enad Global 7 while Zynga continued its acquisition-growth strategy. EA itself was also quite acquisitive on Glu Mobile, Codemasters, Playdemic from Warner Bros and a mobile studio.

And as we entered 2022, there was a sense that activity would cool off and recent deals would be digested, with the games’ market set to slow as the best years in the history of the industry had just passed and year-ago comparables were set to become insanely difficult. And then sure enough in a span of two weeks, the two-largest deals in industry history were announced – Take-Two’s $12.7 billion acquisition of Zynga and then Microsoft’s enormous $69 billion deal for Activision Blizzard.

Opportunism, Not Necessarily a Paradigm Shift

Although there was a lot of buzzword-y hot-takes about these two record-setting deals and what they mean for the future of media and the metaverse, let’s take a step back. As enthusiastic as we are about the future development of the metaverse, the true vision of what is being built towards is still a decade or more away. We have proto-metaverse experiences today, mostly evolving out of the interactive entertainment sector, but we are still a long ways away from this true vision.

If we look at these two large deals, although the metaverse was touted as a rationale for Microsoft’s deal for Activision and cross-platform and IP sharing for Take-Two’s Zynga deal, these were really just opportunistic deals. Let’s start with Zynga.

Zynga was running out of runway for growth very rapidly. The acquisition-growth story of the prior five years or so that was massively successfully was running out of targets as the prime acquisition range of companies had simply been cut bare by so many years of industry consolidation. Apple’s privacy changes to disable IDFA targeting for user acquisition made it exponentially more difficult for the company to launch new games, something it had already struggled with before those changes. And its strategy to build an advertising network and build, as termed by Eric Seufert, a content fortress, just seemed like it was a shot in the dark.

Take-Two, meanwhile, has been struggling to tell a mobile growth story for some time. With uncertainty around its future game release slate and slowing engagement in key live services titles, a big mobile acquisition to juice live services revenue and the ability to discuss lots of mobile IP sharing (Grand Theft Auto, Mafia, 2K sports, etc.) sounds great. But there was nothing in the past that ever kept Take-Two from licensing IP to existing mobile game makers so again, this appeared to be an opportunistic deal for what was appearing an increasingly distressed asset in Zynga. It also followed Electronic Arts’ purchase of Glu for similar reasons.

Similarly, Activision was a heavily distressed asset at the end of 2021 in the wake of wide-ranging internal culture allegations that included sexual harassment and misconduct. The company was also facing production delays in key games including Overwatch 2 and Diablo 4. Whether these two are related is up for debate and only those inside the company can say for sure, but, as the saying goes, where there’s smoke there’s fire.

Microsoft, with a massive cash pile, was able to come in and swoop for the company, paying a large premium to the trading price on the day of announcement but still below the company’s prior high price before the scandals and game delays. CEO Satya Nadella was bullish on the metaverse as a rationale for the deal but let’s be honest – this was a Game Pass deal. This was a deal to get more subscribers on Game Pass, a key, possibly the biggest initiative, for Xbox and overall for Microsoft in their push to build consumer subscriptions to augment their enterprise software leadership.

Is EA Distressed?

Unlike Activision and Zynga, EA does not appear distressed. Although some new mobile games like Apex Legends and the latest edition of Battlefield failed to live up to expectations, EA still has a strong lineup of evergreen live services titles led by sports and Apex Legends and some optionality on the mobile side. But let’s look at the numbers:

At a time when many of its peers are seeing significant growth headwinds, EA is still growing net bookings. Its guidance for fiscal 2023 ending March 2023 calls for growth of 6.5% on top of two prior record years. And this factors in currency headwinds and the exit from Russia and Belarus which combined are shaving about 400 bps from growth. Compare that to Activision, where consensus is expecting bookings to drop 6% in 2022. Take-Two expects bookings to rise 11% in fiscal 2023 excluding Zynga, but that’s after a drop of 4% in the prior year whereas EA is coming off of a growth year.

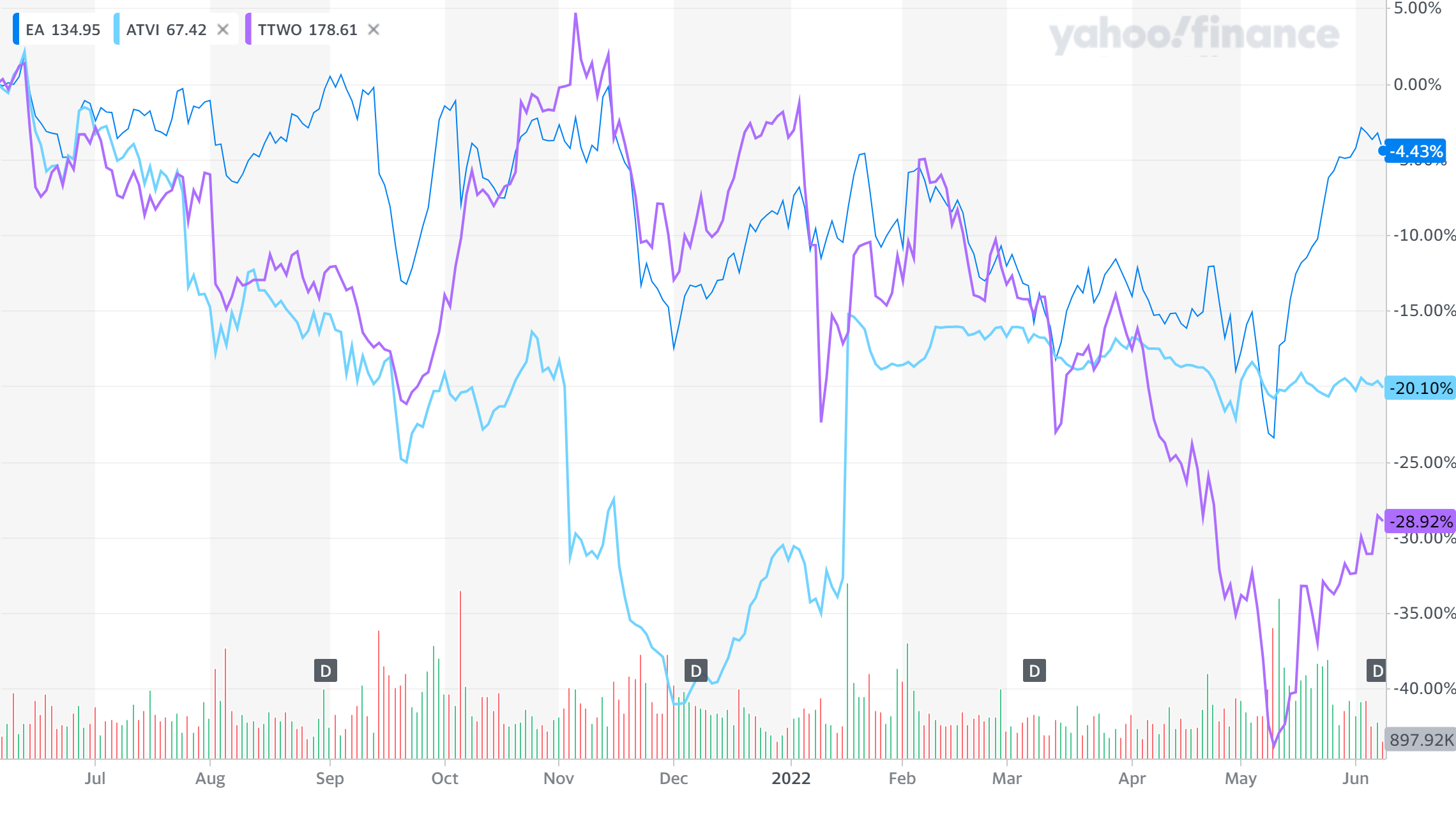

Comparing the share prices of these companies also tells a different story. Before the Microsoft acquisition materialized, Activision’s share price was in free fall, peaking over $100 before bottoming out below $60. EA nearly reached $150 and sold off with the broader sector, bottoming out around $115 but its strong outlook has sent shares back up above $140. Take-Two’s shares that are now around $130 are far below their peak of about $210.

So it doesn’t seem like there’s a distressed, opportunistic situation arising to put EA on the map. It truly does feel different than those deals, that this is just traditional media companies like Disney and Comcast once again spinning the wheels around getting into interactive. It’s largely failed in the past anytime they have, Warner has been the only one to have a modicum of success and that was not without multiple missteps along the way. The new wrinkle is the large megacap tech companies such as Amazon and Apple also potentially getting involved but otherwise it’s more of the same.

So let’s dissect the latest rumors from Puck – that Comcast proposed spinning off NBCUniversal and merging it with EA. This is a similar narrative to the 20+ years of rumors of merging EA with Disney or spinning of ESPN and merging it with EA from a strategic point of view. Sports content, both live, scripted and interactive under one umbrella, and now direct-to-consumer.

Although these deals have strategic merit, they’ll probably fail for all of the reasons that media acquisitions of interactive companies have failed in the past. The folks over at Deconstructor of Fun highlighted four reasons for this that I will just summarize and you can read more from them on:

Game developers don’t want to work for media companies.

Political power in media organizations rests with IP owners, which for the most part has not been the games companies.

Media companies always prioritize the film studios.

It’s incredibly difficult to apply IP licenses to interactive entertainment.

But How Could it Work?

An acquisition of a large game publisher could be successful but would require a large mentality shift from the acquirers on how they would leverage the assets. If acquirers remain steadfast on games meeting film release deadlines as they have in the past, if they jam IP from movies down the throats of developers and they don’t truly value these businesses except as a way to grow film IP, the deals will fail.

But the proliferation of gaming IP in film and TV could be opening up new opportunities to flip the script. Rather than looking at this as a way for game teams to make games around film IP, what if this was looked at as a way to enhance the proliferation of streaming services with more gaming IP.

We’ve seen game-based IP films at the box office and shows on streaming networks such as the Witcher and Arcane be massively successful. Sony is pushing harder on this with its PlayStation Productions to bring out projects such as Uncharted and the Last of Us. So could this work?

Well, EA leans on licensed IP for a lot of its big franchises in sports and Star Wars. So is the value proposition of Dragon Age, Mass Effect, Dead Space, the Sims, Plants vs Zombies and others worth it to justify an acquisition purely from an IP perspective? Probably not. This sort of acquisition probably makes sense for a smaller game companies with unique IP like CD Projekt, not a large diversified publisher like EA.

For a large tech company like an Amazon or Apple, a deal could be justifiable a bit easier – we want to get into games, we have a lot of cash and these games people can do their own thing because in the scope of our total business it’s still kind of immaterial. However, until regulators rule on Microsoft’s deal for Activision, it’s unlikely other deals like that will follow. If it succeeds, I wouldn’t be surprised to see a company of the ilk of Amazon get involved.

So What Does the Metaverse Have to Do With This?

Again, the metaverse is not the rationale for these multi-billion dollar acquisitions and at this juncture it shouldn’t be. But there are some motivations worth considering that over the next few years could become more important strategically for these companies.

There’s a reason the metaverse is emerging from the interactive entertainment sector first – game developers have the most experience with real-time 3d and the metaverse enables real-time 3d everywhere. So for these large organizations to secure talent and technology, particularly for companies like Amazon that have already shown an interest in building their own real-time 3d engines, you can start to paint a story to justify a game company acquisition over time. Media companies should also be considering how they enter the metaverse in the future, but I suspect they will rely more on licensing their IP to leading platforms than building their own for some time.

Eventually, the likes of Disney and Comcast will look to build their own solutions but will probably do it based on off-the-shelf technology. Disney already uses Unreal Engine and Unity for virtual film sets and there’s no reason for them to invest hundreds of millions of dollars over decades to even try to catch up.

For more insight on the rumors swirling around EA, listen to the second episode of This Week in the Metaverse, where Brian Peganoff and I chatted in depth about what it means. And for more on the potential of real-time 3d everywhere, listen to our fantastic conversation with Unity’s Marc Whitten.

If you liked this essay, subscribe below to be the first to read our written materials and listen to new podcast episodes of Into The Metaverse.